Architecture Diagram

The Five Layers

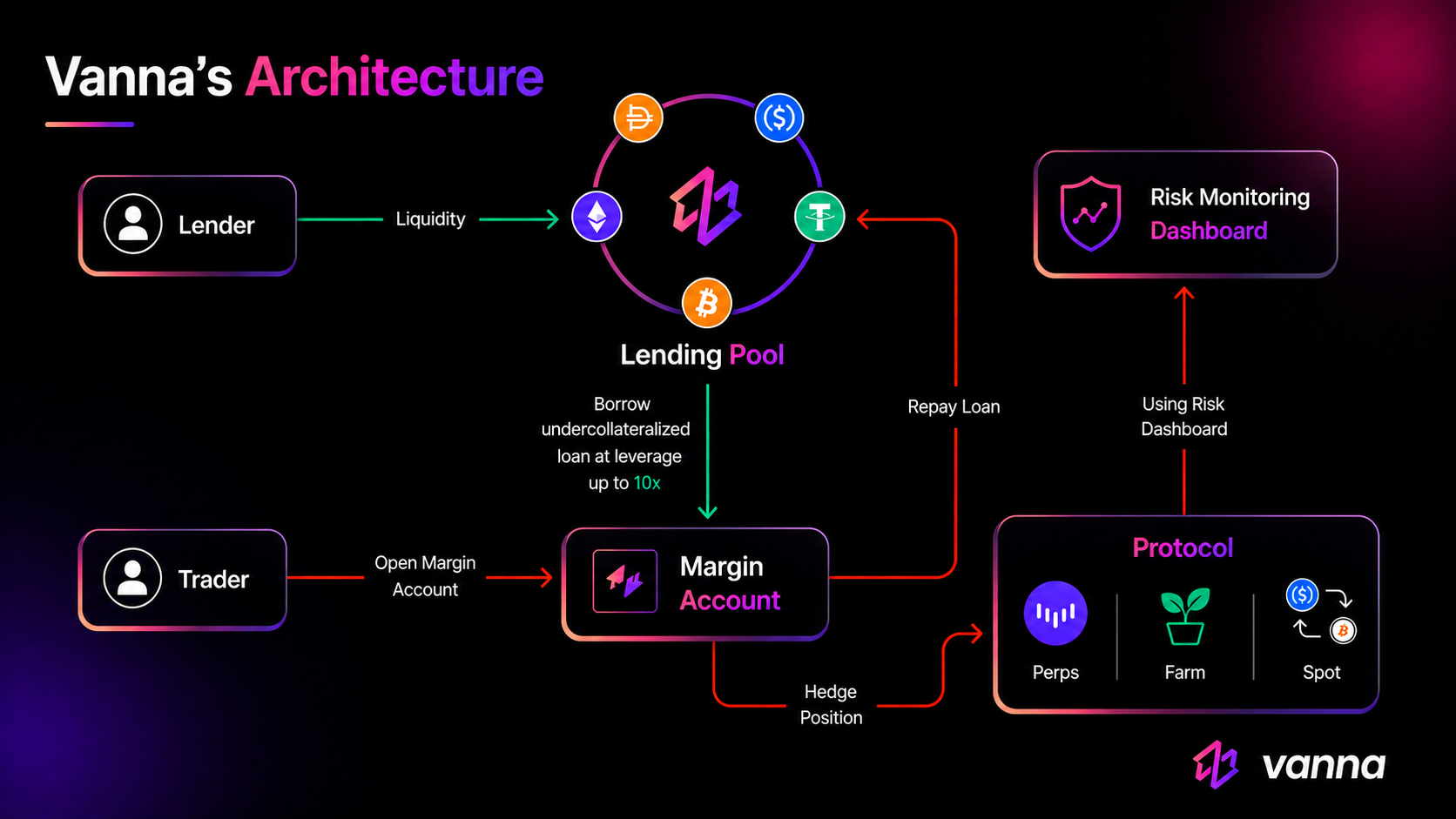

Entry Layer - Account Manager

The Account Manager is the sole entry point for all trader operations: account creation, collateral deposit and withdrawal, borrow, repay, settle, liquidation, andexecute(). It resolves all peer contract addresses from the Registry at runtime. No trader call bypasses it.

Per-User Layer - Margin Account (Smart Account)

Each trader gets a separately deployed contract - not a mapping entry in a shared contract. It physically holds the trader’s collateral tokens, maintains the borrow list, and is the contract that calls Blend or Aquarius when a trader opens an external position. One account’s state cannot affect another’s. Closed accounts are pooled and reused to amortize deployment costs.Lending Markets - Pools and vTokens

Two isolated pools: one each for XLM and USDC. Each pool accepts LP deposits, lends to Margin Accounts, accrues interest via the Rate Model, and mints or burns its corresponding vToken (vXLM, vUSDC). Pool isolation means a borrow shortfall in one asset does not spill into another.Risk Layer - Risk Engine and Oracle

The Risk Engine is the protocol’s gatekeeper. The Account Manager calls it before every borrow, withdrawal, or liquidation. It reads collateral balances from the Margin Account, borrow shares from each Lending Pool, and live USD prices from the Oracle. It caches prices per symbol within a transaction to avoid duplicate oracle calls. If the post-operation health factor would fall below 1.1x, the operation is rejected.Infrastructure - Registry and Tracking Token

The Registry is the on-chain address book. Every contract resolves peer addresses through it at runtime. Upgrading the Oracle or Rate Model requires updating one registry entry, not redeploying dependents. The Tracking Token is a multi-symbol receipt contract. When a Margin Account deposits into Blend or adds liquidity to Aquarius, the Account Manager mints a tracking token representing that external position. The Risk Engine reads these balances to include Blend b-token and Aquarius LP positions in the collateral calculation.The Gating Order

Every state-changing operation follows the same sequence:Call enters Account Manager

The Account Manager authenticates the caller, resolves contract addresses from the Registry, and prepares the operation.

Risk Engine evaluates health

Before any tokens move, the Account Manager calls the Risk Engine. For borrows and withdrawals, it computes what the health factor would be after the operation and rejects if it falls below 1.1x. For liquidations, it checks the current health factor and rejects if the account is still above 1.1x. Either way, the call panics here if the check fails - nothing else executes.

Lending Pool or Margin Account processes the operation

If approved, the Account Manager calls the Lending Pool (for borrows and repayments) or the Margin Account (for collateral changes and execute calls). The pool calls

update_state() first to accrue interest since the last operation.Contract Map

| Contract | Layer | Responsibility |

|---|---|---|

| AccountManager | Entry | Single user-facing entry point |

| SmartAccount | Per-User | Isolated margin account per trader |

| RiskEngine | Risk | Health factor gatekeeper |

| Oracle | Risk | Live asset price feeds |

| LendingPool (XLM) | Markets | XLM lending and borrowing |

| LendingPool (USDC) | Markets | USDC lending and borrowing |

| vXLM / vUSDC | Markets | LP receipt tokens |

| RateModel | Markets | Polynomial interest rate curve |

| Registry | Infrastructure | On-chain address book |

| TrackingToken | Infrastructure | External position receipts |

Go Deeper

Margin Accounts

Per-user contract lifecycle, storage layout, and isolation model.

Lending Pools

Pool accounting, vToken mechanics, and how borrows are issued.

Health Factor

The 1.1x threshold, the three check types, and what moves the ratio.

Composable Leverage

How execute() deploys borrowed capital into external protocols.

Interest Rate Model

The utilization-based polynomial curve that prices every borrow.

Oracle System

How asset prices enter the Risk Engine and what happens on failure.